“Post-Venture” Capital and the Crypto Nobel Prize

An experiment with innovation on the blockchain.

I should write this essay as an inspiring speech. I should confidently tell you about the new world we’re building with my organization, Planck, and how it will change everything. I should show charts, letting you behold the enormous addressable markets that we will conquer.

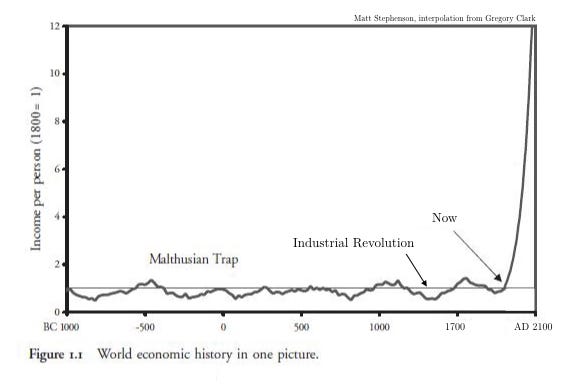

Unfortunately, I can’t do that here. I’d be standing next to a chart, something like:

“This is a picture of the last time humanity solved a core innovation problem” I’d say (truthfully.)

But as you can see, that’s an addressable market so big that even the most exuberant, skyward-gazing pitch couldn’t discuss it with a straight face. And to make matters worse, I’m trained as an academic. (I must ask, then, that you mentally append some awful clause — let’s go with “according to some, it might be possible that” — to every sentence in the whole article. Thanks in advance.)

But it’s true: as far as economists can tell, the addressable market for innovation itself is perfectly equal to economic growth (per person). This is all the wealth that gets created in the world and it’s somewhere around 5 trillion dollars a year, all due to innovation. New ideas, new knowledge, and new ways of doing things — what economist Paul Romer calls “new recipes”.

Innovation is new wealth. As a result, any project working on incentives for innovation itself has this trillion dollar monstrosity as its market. And yet when I say that Planck is trying to help scale scientific innovation, you probably don’t think about a trillion dollar market.

But science is just a decentralized protocol for innovation — it structures and rewards shared knowledge. And so if blockchain is going to transform innovation, massively scaled open science is probably what it will look like. This has already been unbelievably valuable — imagine if you had to pay a physics tax, or if you had to sum up the wealth that Alan Turing created in the world.

The Industrial Revolution, that historical explosion of wealth we saw in the graph earlier, was a radical shift to open innovation. As economic historian Deirdre McCloskey puts is, “what made our world astonishingly rich” in this period is that:

Poor people such as the blacksmith John Harrison (marine chronometer) or the son of a weaver John Dalton (atomic theory, among other ideas) or the seamstress Coco Chanel (business attire for women) were permitted for the first time in history to innovate.”

But today, growth is slowing among countries at the “technological frontier.” And developing countries are slowing as they catch up. Have we really maxed out innovation, as some economists think? Are there great ideas left to find?

How do we reward innovation today?

Or: the problem with “planting crops is worth nothing; only harvesting matters”

There is a reason why venture capitalists say “Ideas are Worth Nothing; Only Execution Matters.” It’s, first and foremost, a solid joke.¹ But it’s also true in a very deep sense: a shared idea can’t be protected. In Elinor Ostrom’s terms, a shared resource that you can’t protect is a “non-excludable public good”. And this inability to protect valuable, scarce resources produces the infamous tragedy of the commons.

It’s absolutely true then that, conditional on telling the world your ideas, ideas are usually worth nothing. And this is nobody’s fault. The fact is, VCs and Angel Investors focus on execution because the marketplace for ideas has very, very poor economics.

Just how bad are the economics for new ideas? Peter Thiel (w/ Blake Masters) gives an example:

In the 1980s you could build a better disk drive than anybody else, you could take over the whole world and two years later someone else would come along and replace yours. [This] had a great benefit to consumers, but it didn’t actually help the people who started these companies.

Thiel’s describing a breakdown in the rewards for innovation in microelectronics. That is, he’s talking about an industry with crystal clear commercial applications! If it’s hard to reward innovation there, imagine trying to fund “antifragile tinkering” in cryptography (i.e. the innovations from the 70s and 80s that Bitcoin used).

These lessons were learned quickly by Wall Street. Any company running an open research lab like Bell Labs was, by the 1980s, thought to be displaying “managerial negligence”.² The corporate research labs that remained became much more secretive by necessity, and their productive knowledge was protected and silo’ed.

The decline of research incentives has serious consequences though. Consider a crucial driver of the economy like Moore’s Law: over the past few decades, innovation productivity on Moore’s Law has declined by a factor of 18. Moore’s law is, today, sustained by massive armies of researchers.

This is the economic reality of “Ideas Don’t Matter; Only Execution Matters.” It’s a world in which you increase horsepower not by building a car, but by adding thousands of horses to pull a carriage.

Why Post-Venture Funding Matters

It’s usually hard to tell who will benefit from a great innovation. For instance, Albert Einstein’s equations are essential for GPS devices, but at the time there were no GPS companies. Who should have funded him?

As it happens, Einstein had to fund himself. But he knew he was at least working for something — science has a strong tradition of attribution and citation and, at the very least, Einstein knew would he would be credited. But even this minimal standard is very hard to enforce.

As a “back of the envelope” test of this idea, I Googled some popular concepts in crypto with and without the author’s names. Then I divided the results to produce a citation rate — how often people use the content and mention the author.³ It’s a not much of a study, but it does tell a story I think many would recognize:

I don’t know any of these authors (not very well, anyway) and they might not care at all about being cited. But I suspect that it’s better to create an “opt-out” system for this. And click-maximizing content aggregators certainly don’t help things. Attaching a thought leader’s name to a new concept probably maximizes eyeballs and clicks, as you can see below:

In the above example Leslie Lamport needs to rely on a very busy person to help ensure credit (worse still, it may not really be in Vitalik’s interest to correct the record like he did.) We can do better.

How Blockchain Helps

Fortunately, blockchain is an exceptional technology for rewarding innovators and early adopters. And what we call “post-venture” funding — rewarding people for what they’ve already done or created — has recently exploded on platforms like Twitch. For instance, Streamlabs estimates that donations to Twitch streamers totaled over $100 million in 2017.

In the knowledge economy Planck wants to help bolster, this is like “post-venture” capital. Science works by creating competition for “priority”, thereby encouraging people to relinquish credible, valuable knowledge— in open science, creating and sharing knowledge is the venture itself. And of course, after the idea is publicly shared, normal venture capital should go to the person who can best execute on it. That’s as it should be. But post-venture capital is backward looking; it commits to rewarding what’s already been ventured.

We believe that this has the potential to make the innovation process vastly more efficient. A more effective division of labor between the best innovator and best executor can change the world.

Genius Grant Futures for Money and Attribution

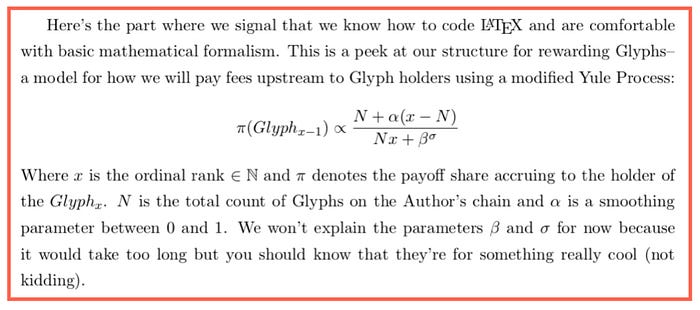

We explain technical details of how our prizes and our Non-Fungible Tokens (called Glyphs) work in our whitepaper, but here’s a brief sketch:

Prizes are commitments to reward great ideas. Anyone can create a prize, everything from our Blockchain Genius Grant, to “Matt’s Personal Top Ten Favorites of The Year.” And by creating and maintaining a periodic prize, you are committing to help build a world in which innovators are rewarded.

Prizes are not just awards on Planck; they are exchanges. The effect of this is to mix natural human reciprocity with investment in the possible future manuscript value of the Glyph itself. A prize gives cryptocurrency in exchange for a Glyph. Why might Glyphs have value?

- Historically, great knowledge is valued like great art. Bill Gates paid $40 million for Leonardo Da Vinci’s Codex Leicester. Einstein’s manuscripts sell for millions. And a single page of Darwin’s writing fetches hundreds of thousands of dollars. While you may think there’s some aesthetic beauty tied into that valuation, the ideas can even be typed — James Naismith’s original typewritten Rules of Basketball recently fetched $4 million in an auction. People buy Darwin’s original pages because they are connected to his idea — the fact that information from The Origin of Species is freely available is not a bug for its high value; it’s a feature. Today’s Darwin would type The Origin of the Species in a Google Doc or a versioned LaTeX file or a post on Medium. But now with Planck, and the digital scarcity blockchain enables, she would create a unique Glyph that serves as that first manuscript copy.

- Glyphs also entitle the bearer to upstream rewards from the creation of new Glyphs (in the same chain). This is a little complex for an intro article, but intuition for this structure can be found in Chris Dixon’s excellent “Why Decentralization Matters” as well as Steemit and Simon de la Rouviere’s thoughtful work on Bonding Curves (Bruce Kogut was my formal introduction.) Innovations like Harberger taxes are also very relevant here.⁴ At any rate, feel free to skip this little semi-technical preview into the structure we’re encouraging:

Because owning a Glyph may get you revenue and collectable value, it can pay to buy them and hold them even beyond rewarding an author. This possible payoff means a reduced risk for the very early investors, such that more value can safely flow upstream to the author in multiple ways. At the very least, this should all help ensure attribution for the original idea since each Glyph contains a citation of the original work.

Planck can also enable prizes on prizes, “rewarding the rewarders” of innovators. That can happen if an innovator succeeds and wants to pay back the people who helped them early by buying back their Glyphs. It can also happen when we see someone rewarding others, such as when the anonymous person behind the Twitter account @tether_is_fiat helped reward the important blockchain elder statesman Andreas Antonopoulos.⁵

Anyway though, maybe you’d prefer the meme explanation at this point: Planck is kind of like a tokenized Patreon crossed with an auction house, but for knowledge.

Conclusion: The Blockchain Science Stack

As we discussed, science is a protocol for structuring and rewarding new knowledge. If you’ve read this article picturing some sweaty philosopher in a basement hoping to make 2 bucks you’re not thinking big enough. Science is the decentralized structure. Scaling it, well… innovation is valued annually in the trillions, remember. If you’re business-innovation-minded, here are a few “shower thoughts” that might pique your interest further:

- Are there incredibly innovative people who are too busy to work on all their ideas? Are there great innovators who might be overextended as executors? If so, maybe we wish that we could get them to share more ideas openly. Incentives matter.

- Would companies like to have a global suggestion box? If they publicly commit to refunding most glyphs created for them, they can get lots of suggestions (while still avoiding spam because of the Glyphs’ cost.). And if the company commits to handsomely rewarding the Glyphs that they actually use, they might get a flood of useful ideas.

- Are there people who could establish a reputation for innovation, and then exchange their new, encrypted, ideas for money? These people who could provide encrypted seed ideas that others pay them to reveal, but they could also provide creative solutions as businesses are built and developed.

- Could a large network monopoly be convinced to reward smaller experiments? If enough people had Glyphs staked in new tech experiments, perhaps a large network monopoly that “adopts” that technology would be compelled to make many of them whole. This is likely much more efficient from the perspective of the economy, and it’d be a worthwhile (by definition) marketing cost for the monopoly.

Ultimately, we believe that opening up science is the next step toward a more innovative future. It should be clear that we think of science broadly — but we take its values and methods very seriously.

If this was a grand speech, I might close by asking you to think about whether we might be standing on the precipice of an entirely new world. And perhaps I’d return to the graph at the beginning, pointing out what it might look like to historians of the future if we were to address more of the problems that lie at the core of innovation itself:

But this isn’t a grand speech. Instead it’s an experiment; a small step in what seems like the right direction, drawing heavily on the diligent work of others. We hope we can reciprocate.

We have much, much more. Our whitepaper is more technical, and it does a lot more citing (obviously) but Medium is not conducive to either, so please forgive us in the meantime. We need to thank one notable (but here, anonymous) old-school VC investor for some ideas, along with Denis Nazarov, Wendy Xiao Schadeck, Gareth Jefferies, and Nathan Chen. Important direct inspirations in the crypto world (that we can think of now) are the “Colored Coins” project, ConsenSys, Mediachain, Dieter Shirley, Ascribe. Academically/intellectually we owe a special debt to Bruce Kogut, Richard Nelson, Stephan Meier, Eric Abrahamson, Andrea Prat, Vernon Smith, Toshio Yamagishi, Dani Rodrik and Elinor Ostrom. There is a lot of high quality non-academic writing and podcasting as well that we cite in our whitepaper. If there are other projects and people we didn’t mention or left out we apologize. We are solely responsible for any and all errors.

Endnotes

[1] More precisely “ideas are worth nothing” is a Koan, like “What is the sound of one hand clapping?” To see this, just consider that “ideas are worth nothing” is itself an idea.

Of course, when a Venture Capitalist says “Ideas are Worth Nothing” it’s a sort of shorthand. It means: “here you are talking to me, a VC. That means that you need to openly discuss your ideas to get them done. But when people openly discuss their ideas, anyone can use them. And when anyone can use an idea, only execution on the idea matters.”

[2] This is from Philip Morowski’s Science Mart. Morowski is being critical but ultimately I think he would agree that it is unprofitable to run an open research lab in a world where, say, positive research externalities extended far beyond the national boundaries of effective risk pooling.

[3] I assume they are the authors anyway! This is a big part of the problem. If you can rely on others citing properly then you only have to cite a few things. If not, well, it’s a tough road. See, for instance, our whitepaper which has about 40 cites where we just took our best guess.

[4] Simon de la Rouviere wrote a piece about Harberger taxes for NFTs which is very good. To my knowledge Glen Weyl and Eric Posner popularized the Harberger concept.

And if you’re down here reading the footnotes like a good Straussian, we might as well tell you that we’ll be writing a follow-up on the science of innovation. In our estimation, the existing evidence shows that innovation responds to incentives, which would mean that — given the well-known incentive problem discussed above (originally formalized by Richard Nelson and Ken Arrow) — we currently have an under-provision of valuable knowledge. I think that’s almost certainly the case.

The innovation process itself, in the individual, isn’t well-understood at all. It seems to have something to do with intuition — for instance, Stephen Wolfram is very eloquent in describing Ramanujan’s incredible aesthetic sense for the “mathematical facts” that mattered. At any rate, thinking very hard about a topic in an area you understand, then imposing some formalizing process on your thoughts (mathematics and real-world tinkering are often used to great effect) often yields a kind of progress. It’s a really special thing, or so we’ve been told.

[5] The story as we understand it is this: Andreas was involved in Bitcoin very early, but he had always used his cryptocurrency and was thus not nearly as wealthy as those who invested and held. The anonymous t_i_f began a kind of “post-venture” round that eventually raised over $1 million for Andreas, rewarding him for all of his work. It was a really great thing to see. And while we don’t know t_i_f’s story, we might like to reward her for her actions as well. Certainly if she’s in need but even if not — ultimately we are putting cryptocurrency in the hands of a person who used it well (by rewarding a linchpin of the community.)